When A Toll Isn’t A Toll

By Benjamin Picton, senior market strategist at Rabobank

When A Toll Isn’t A Toll

Yields on 10-year Treasuries finished last week up 11bps to 4.48% while yields on 10-year Bunds rose 8.5bps to 2.93%. Those higher borrowing costs came despite signs of weakening in the US jobs market, a weaker-than-expected prices paid figure on the ISM manufacturing index, and a surprisingly weak Eurozone CPI inflation report that follows in the wake of lower than expected inflation readings in the UK.

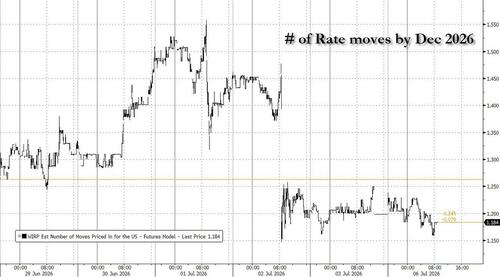

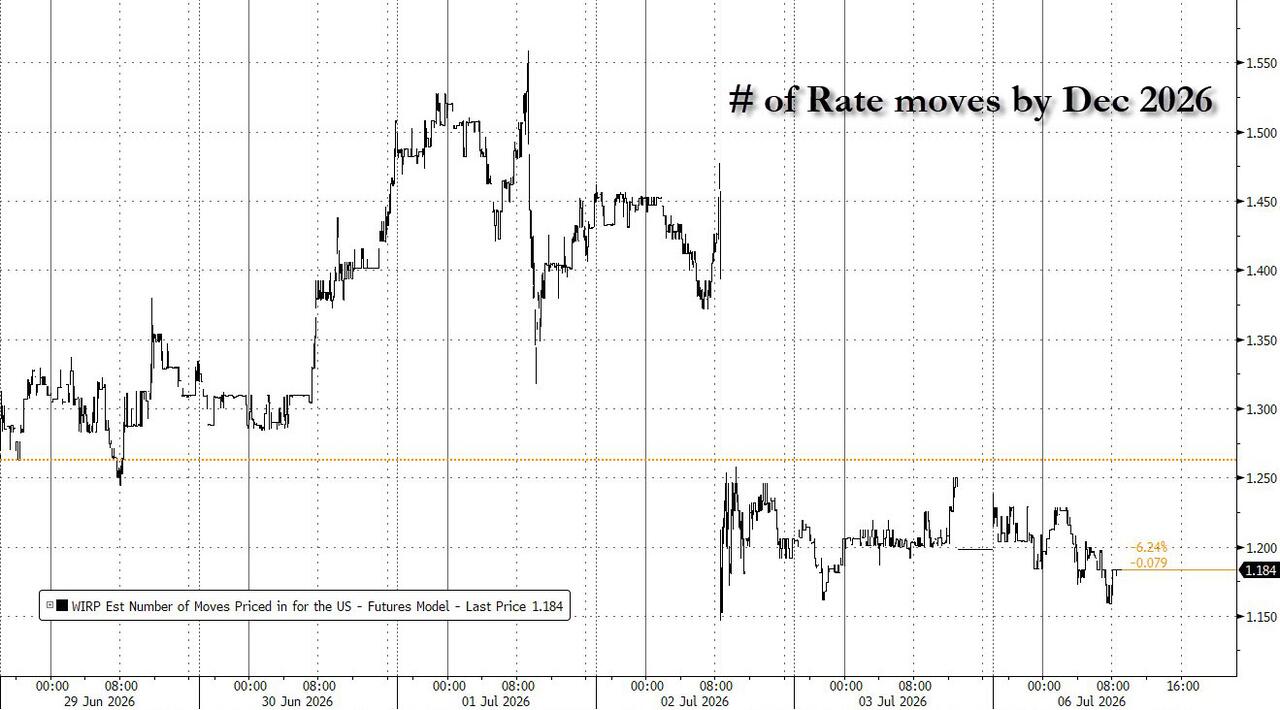

Market-based expectations of the future path of the Fed Funds rate finished the week a little lower than it started, with pricing of a future rate hike pushed out from October to December. 2-year Treasury yields fell by almost 4bps on Thursday after the payrolls report confirmed hiring in June was little better than half the expected figure.

This was still enough for the unemployment rate to tick down to 4.2% as a lower participation rate saw the labor force contract. Nevertheless, 2-year yields were higher across the week as sovereign curves bear-steepened.

Brent crude posted its first weekly gain in almost a month last week to see the front contract close up 0.18% at $72.12/bbl. The gains appear to have been short-lived as news of continued tanker flows through the Strait of Hormuz and a decision by OPEC+ over the weekend to ease production restrictions by 188,000 barrels/day from August steer the price action lower this morning. Announcements of increased production are all well and good, but when much of that production is occurring in the Persian Gulf or in Russia (where Ukrainian strikes against oil infrastructure are ongoing) the ability to actually ship the product to market will remain the critical limiting factor.

On that note, official figures show that Hormuz traffic is back to approximately 30% of pre-war levels, though this likely understates the true picture as many vessels are transiting dark (i.e. without their tracking systems on) to avoid the attentions of Iran’s IRGC. Bloomberg reports that six vessels transited the route closest to the Omani coastline under US auspices on Sunday without incident. That follows reports of up to eight vessels performing u-turns (with some later being redirected through the Iranian route) after attempting to transit close to Oman on Friday and Saturday.

Updated data from Kpler and Vortexa shows that crude exports from the UAE surged in June to exceed pre-war levels and approach record highs. The UAE’s recent decision to leave OPEC and OPEC+ is considered bearish over the longer term for energy prices as a diminished share of potential production is subject to non-market constraints.

On the other hand, Iran again indicated over the weekend that it will be instituting “service fees” on vessels transiting Hormuz through its territorial waters once the 60-day negotiating period kicked-off by the signing of the Iran-US memorandum of understanding expires. According to Iran’s ambassador to China a new fee regime is being designed in consultation with Oman and will include “special considerations” for China and other friendly nations in determining the level and type of fee applied. According to the ambassador, this is not a toll. This might prove be a convenient fiction for all parties given President Trump’s unyielding view that a permanent toll regime would not be acceptable after the 60-day negotiating period expires.

Critically, what this little titbit sets up is exactly the type of scenario we have been pointing towards for some time: the ‘oil market’ splitting into ‘oil markets’ with terms over pricing and access being determined by which geopolitical camp you happen to sit in, and a series of quid pro quos informing the deal that each party gets.

The prime movers here are the United States and China, with Iran having clearly chosen China and the UAE hitching its wagon to the US of A. An easy tell that this scenario is playing out will be pressure from Iran to have other Gulf producers accept a toll that isn’t a toll, and/or have their cargoes priced in CNY rather than USD. The USA, similarly, will pressure Gulf allies to price in Dollars and normalize relations with Israel to expand the Abraham Accords and have oil flow from east to west to cut out Iran entirely and demonstrate to China that Uncle Sam can step on the hose whenever he likes.

Europe and the balance of Asia are likely to be reduced to the role of spectators in these affairs. Highlighting the weakness of Europe’s current position in the Great Game, the Wall Street Journal carried a story last week on how the German Mittelstand is being decimated by state-backed Chinese competition, with the most energy-exposed sectors of the manufacturing economy faring particularly badly.

To a certain extent, the hollowing out of German industry at the hands of China mirrors the hollowing-out of British finance at the hands of the United States as more and more firms choose to list in New York in pursuit of higher multiples or are bought-up as value picks. This has elicited a response from the British Government in the form of the Mansion House compact aimed at encouraging pension funds to hold more British assets. If that fails, will the discussion then turn to capital controls under an Andy Burnham premiership?

Similarly, the rapid decline of the German Mittelstand will almost certainly elicit further protectionist measures from officials in Brussels who have just spent the last 18 months and more criticizing Washington for taking similar steps to protect American industry. In the absence of a hold-your-nose peace accord with Russia to reduce energy costs that will almost certainly not happen, what is Europe’s grand macro strategy to avoid being de-industrialised by China and vassalized by US energy and finance?

Tyler Durden

Mon, 07/06/2026 – 09:15