“All Systems Go”: Goldman Sees Improvement As Boeing Turnaround Gains Momo

Boeing shares jumped as much as 5% after the company posted a smaller-than-expected first-quarter cash burn and delivered the most aircraft since 2019 (outdelivered Airbus for the first time in years), reinforcing the view that the turnaround is beginning to lift off. The CEO’s earlier comment was “all systems go,” while Goldman’s initial read on the quarter pointed to “improvements.”

First-quarter earnings results show Boeing is gaining traction and is set to ramp up 737 production, a key step toward restoring its cash cow narrowbody jet production …

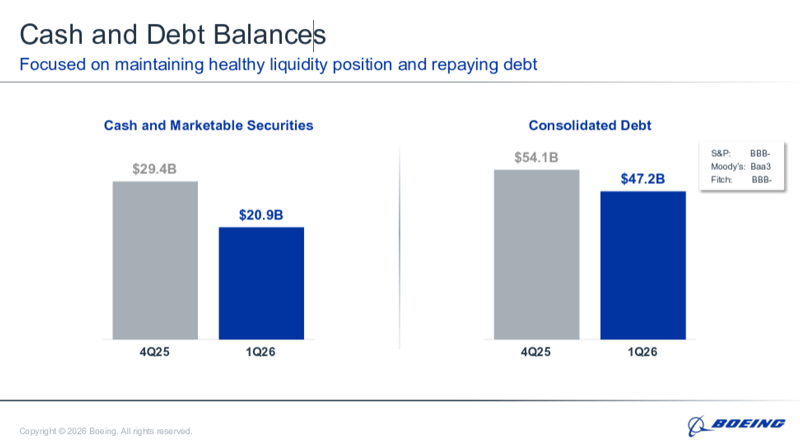

… and reducing debt by $7 billion.

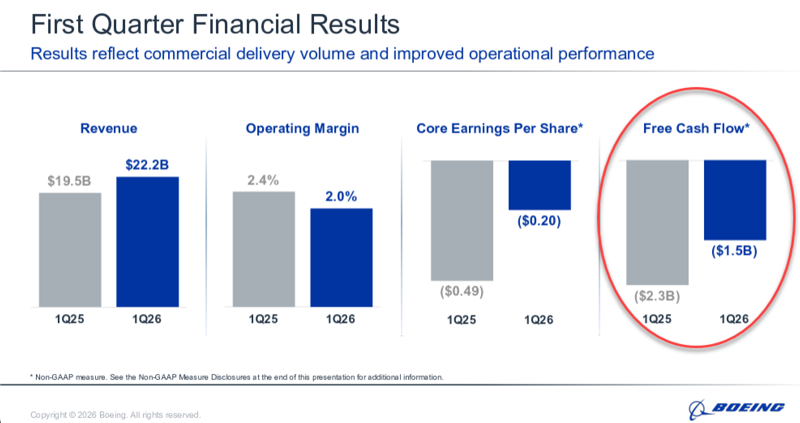

The company reaffirmed its expectation of generating $1 billion to $3 billion in free cash flow in 2026, while adjusted losses were narrower than forecast.

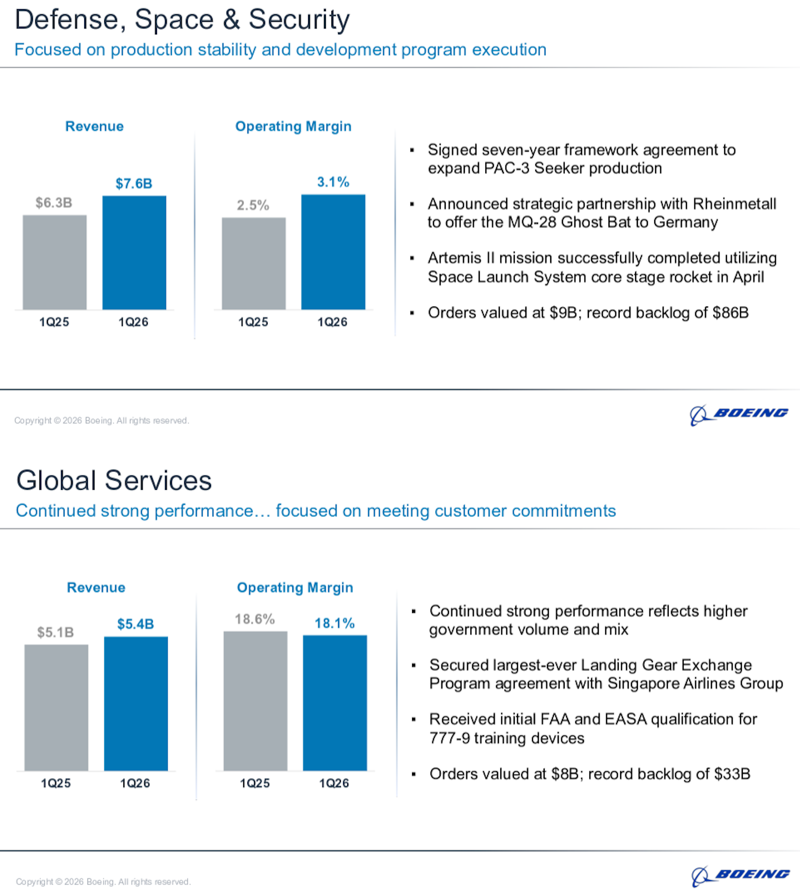

Additionally, Boeing’s defense and space units improved, with revenue up 21% and margins increasing.

“We’re making strides to strengthen our culture and restore trust with our customers while growing our record backlog to nearly $700 billion,” CEO Kelly Ortberg wrote in a message to employees.

Ortberg joined CNBC’s “Squawk on the Street” after the earnings report and said, “All systems are go.” He noted that there has been no slowdown in aircraft orders since the US-Iran war began in late February.

Shares were up as much as 5% earlier in the session but were trading closer to 4% by around noon. Even with today’s move, the stock is only modestly higher on the year, up about 5.2%. The bigger picture is that Boeing shares have remained stuck in a six-year trough following the two fatal 737 Max crashes, which capped production.

A break above $250 would mark an important technical point that could unlock upside momentum.

Goldman analyst Noah Poponak’s first take on Boeing’s quarter was broadly constructive:

Boeing Co. (BA): 1Q26 First Take: Improvements

Bottom line: BA 1Q26 results include revenue and free cash above consensus, improving defense margins, evidence of ability to keep moving higher in commercial aircraft rate, and further advancement in aircraft certification timelines. 2026 free cash flow guidance is reiterated. We see no clear incremental negatives, and there are a few incremental positives.

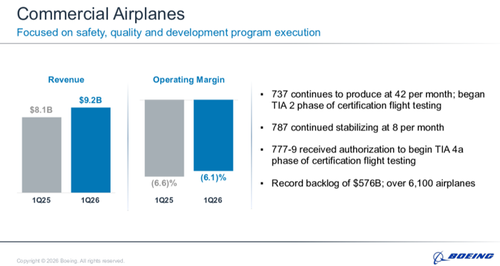

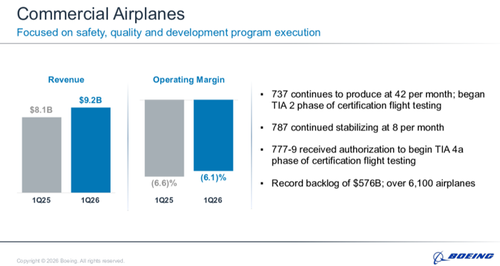

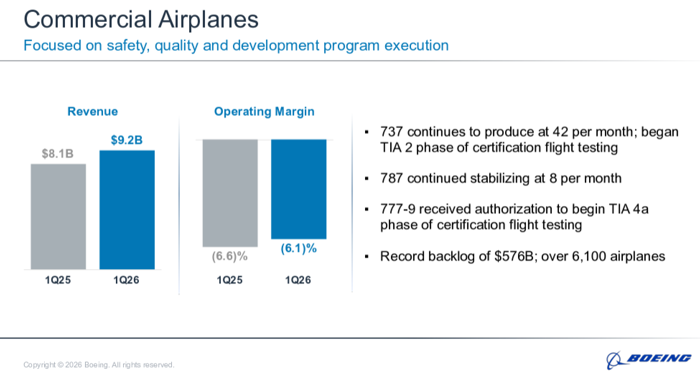

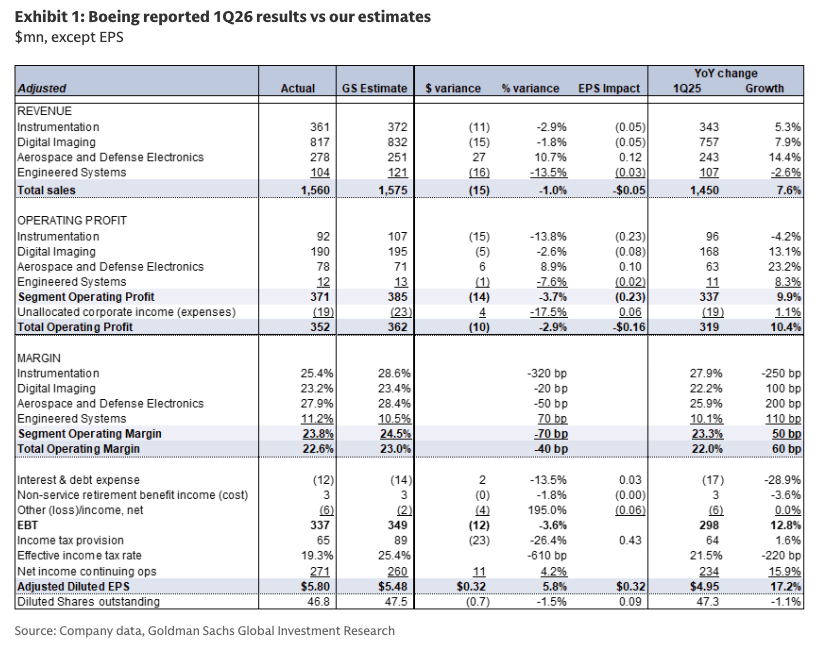

Details: Revenue of $22.22bn is above FactSet at $21.85bn. BCA segment operating income of $(563)mn compared to our estimated $(699)mn. BDS margin of 3.1% compares to our 1.8% estimate. 1Q26 free cash flow is $(1,454)mn, ahead of our estimate of $(2,800)mn and consensus at $(2,340)mn. The company is advancing the 737-10 through FAA Type Inspection Authorization (TIA) flight testing, with certification for both the 737-7 and 737-10 targeted for 2026 and initial deliveries scheduled for 2027. The 777X program has progressed to TIA Phase 4a of certification flight testing for the 777-9 with first deliveries anticipated in 2027.

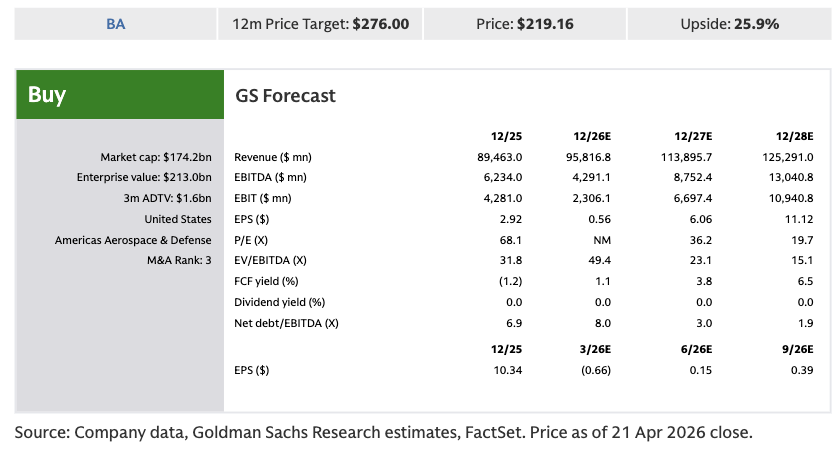

Our 12-month price target of $276.

Separate institutional commentary (courtsey of Bloomberg):

JPMorgan, Seth M. Seifman (overweight; PT $270)

Says cash flow came in better than expected, noting that advances were a key component

“With solid numbers and less exposure to the Iran war than aftermarket names, we assume this will be well-received”

Jefferies, Sheila Kahyaoglu (buy; PT $295)

“A solid, no drama print” with first quarter free cash flow significantly above expectations

Notes that Boeing did not provide 2026 guidance in the release, but previously spoke to a free cash flow inflow of low single digits in 2026

TD Cowen, Gautam Khanna (buy; PT $250)

- Notes that core EPS loss was better than expected, with “BA deliveries and margin slightly agead of BA’s late Q1 guidance update”

Deutsche Bank, Scott Deuschle (hold; PT $223)

Says free cash flow beat was driven by higher operating cash flow, which benefited from a combination of higher net income, favorable advances and accounts payable that helped offset headwinds on inventory

“This print is generally ahead of both sell-side expectations and our sense for buyside expectations”

Bloomberg Intelligence, George Ferguson

- Boeing’s turnaround of commercial airplane was slowed by the necessary purchase of Spirit Aerosystems and will require $5-$6 million cost improvement per fuselage to counter”

All eyes are on the $250 technical break.

Tyler Durden

Wed, 04/22/2026 – 13:40