Foreign Treasury Selling Is Getting Serious

Submitted by QTR’s Fringe Finance

We already knew that the bond market was starting to call bullshit on America’s fiscal and monetary policy. Now we know that foreign governments are dumping U.S. Treasuries, and China is leading the way…even while President Trump pals around with President Xi Jinping.

According to CNBC, foreign holdings of U.S. government debt fell sharply in March as central banks sold Treasuries to defend weakening currencies during the geopolitical and energy shock tied to the escalating Middle East conflict.

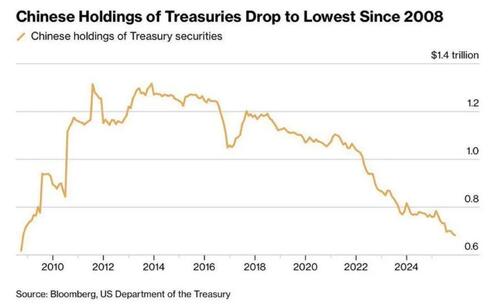

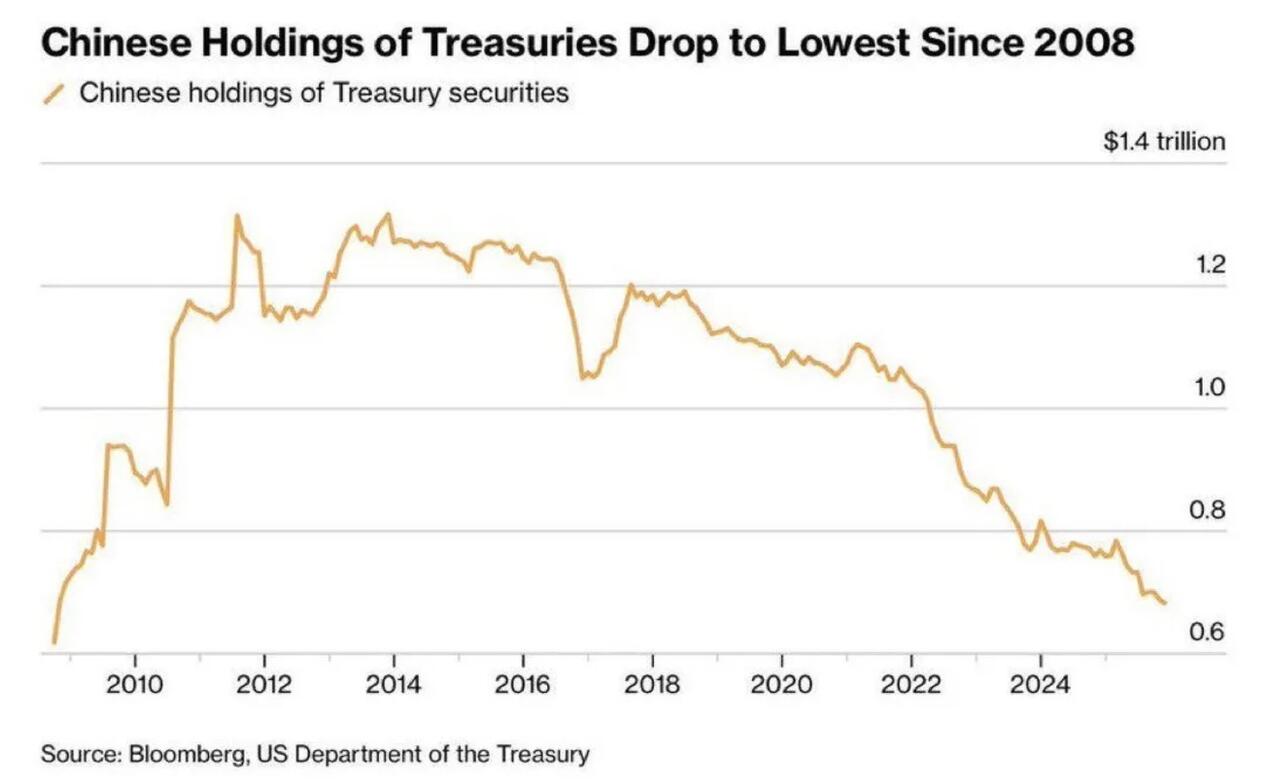

China reduced its Treasury holdings to roughly $652 billion, the lowest level since 2008. Japan, the single largest foreign holder of U.S. debt, also cut exposure aggressively. Overall foreign holdings dropped from approximately $9.49 trillion to $9.25 trillion in a single month.

That should deeply concern anyone paying attention to the structural fragility underneath the U.S. financial system.

For decades, the global economy has operated on a relatively simple arrangement. The United States issues the world’s reserve currency, foreign governments recycle trade surpluses into U.S. Treasuries, and America finances massive deficits because the rest of the world willingly absorbs its debt. That system only works as long as there is confidence in the dollar, confidence in the Federal Reserve, and confidence that U.S. government debt remains the safest and most liquid place on earth to park capital.

When major foreign holders begin reducing exposure during a period of rising inflation, exploding deficits, and growing fiscal instability, it creates a potentially dangerous chain reaction. And the timing for the world to be dumping treasuriers right now could not be worse.

Bonds are already under pressure because inflation is proving far stickier than policymakers expected. As I wrote last week, both CPI and PPI came in significantly hotter than anticipated, forcing markets to rapidly reassess the possibility that the Federal Reserve may actually need to raise rates again instead of cutting them.

Meanwhile, deficits continue spiraling, interest expense on the national debt keeps exploding higher, and the Treasury must issue enormous amounts of new debt simply to keep funding government spending. Now layer weakening foreign demand on top of all of that.

That combination is nasty. If foreign governments buy fewer Treasuries while supply continues surging, yields move higher. Higher yields tighten financial conditions across the entire economy. Mortgage rates stay elevated. Corporate refinancing becomes more expensive. Regional banks sitting on massive unrealized bond losses face renewed pressure. Commercial real estate weakens further. Consumers get squeezed harder.

And because Treasuries serve as the foundational collateral layer of the global financial system, instability there spreads everywhere else. This is why the liquidation story matters far beyond geopolitics.

China reducing Treasury exposure is not entirely new. The broader trend has been developing for years as Beijing slowly diversifies reserves away from direct dependence on U.S. assets. Whether through outright selling or indirect “shadow holdings” routed through financial centers like Belgium and Luxembourg, the direction has been fairly clear for a long time.

But Japan selling aggressively alongside China is where things become even more uncomfortable. Some of Japan’s selling is likely tied to defending the yen as energy shocks and rising oil prices pressure its economy. Japan imports the overwhelming majority of its energy, so a collapsing yen combined with surging import costs creates enormous strain domestically. Selling Treasuries gives Tokyo access to dollar liquidity it can use to intervene in currency markets and stabilize the yen before the situation spirals further.

Japan has spent decades as one of the most reliable buyers of U.S. debt. If even Tokyo is becoming less comfortable absorbing massive amounts of Treasuries while inflation remains elevated and deficits continue exploding, markets should pay attention. Japan may simply see the same thing the bond market increasingly sees: the United States is issuing debt at an unsustainable pace into an environment where inflation is no longer fully under control.

If that’s the case, that is not just a portfolio adjustment. That is a confidence signal. The uncomfortable reality is that the United States has become dangerously dependent on perpetual debt expansion at the exact moment global appetite for absorbing that debt is becoming less certain.

🔥 50% OFF FOR LIFE: Using this coupon entitles you to 50% off an annual subscription to Fringe Finance for life: Get 50% off forever

And this is where the Federal Reserve’s trap becomes even more severe. If inflation reaccelerates while Treasury demand weakens simultaneously, the Fed faces two terrible options: raise rates further to defend credibility and contain inflation, risking deeper stress across banks, housing, private credit, equities, and the broader economy or step back in with liquidity programs and money printing to stabilize markets and absorb debt issuance, effectively reigniting the same inflation problem they spent years trying to contain.

That is the corner policymakers have backed themselves into after years of artificially suppressed rates, endless stimulus, and the assumption that global demand for U.S. assets would remain infinite regardless of fiscal discipline.

It won’t. And I wrote this past week about why it seems incoming Fed Chair Kevin Warsh has a job in front of him that seems impossible.

The most dangerous part of this story is that markets still seem unwilling to fully process what sustained deterioration in Treasury demand would actually mean. Investors have spent decades treating U.S. government debt as the unquestioned risk free foundation of the financial system.

But when foreign governments begin reducing exposure while inflation stays elevated and deficits spiral, that assumption starts getting tested in real time.

And once confidence in the system itself begins eroding, things can unravel far faster than policymakers would like to admit.

—

QTR’s Disclaimer: Please read my full legal disclaimer on my About page here. This post represents my opinions only. In addition, please understand I am an idiot and often get things wrong and lose money. I may own or transact in any names mentioned in this piece at any time without warning. Contributor posts and aggregated posts have been hand selected by me, have not been fact checked and are the opinions of their authors. They are either submitted to QTR by their author, reprinted under a Creative Commons license with my best effort to uphold what the license asks, or with the permission of the author.

This is not a recommendation to buy or sell any stocks or securities, just my opinions. I often lose money on positions I trade/invest in. I may add any name mentioned in this article and sell any name mentioned in this piece at any time, without further warning. None of this is a solicitation to buy or sell securities. I may or may not own names I write about and are watching. Sometimes I’m bullish without owning things, sometimes I’m bearish and do own things. Just assume my positions could be exactly the opposite of what you think they are just in case. If I’m long I could quickly be short and vice versa. I won’t update my positions. All positions can change immediately as soon as I publish this, with or without notice and at any point I can be long, short or neutral on any position. You are on your own. Do not make decisions based on my blog. I exist on the fringe. If you see numbers and calculations of any sort, assume they are wrong and double check them. I failed Algebra in 8th grade and topped off my high school math accolades by getting a D- in remedial Calculus my senior year, before becoming an English major in college so I could bullshit my way through things easier.

The publisher does not guarantee the accuracy or completeness of the information provided in this page. These are not the opinions of any of my employers, partners, or associates. I did my best to be honest about my disclosures but can’t guarantee I am right; I write these posts after a couple beers sometimes. I edit after my posts are published because I’m impatient and lazy, so if you see a typo, check back in a half hour. Also, I just straight up get shit wrong a lot. I mention it twice because it’s that important.

Tyler Durden

Thu, 05/21/2026 – 08:45